Most of us have become very familiar with GST, that is, Goods and Services Tax, because of its prevalence in the news. The new GST law was brought into operation only in this decade, after much negotiation and debate. Its objective was to simplify the conduct of business.

However, the Income Tax (I-T) provisions make headlines only during Budget season or when there is a raid. It is very important for all Indians who earn an income to be well aware of the I-T Act and procedures.

The Finance Ministry made some important changes to the Income Tax Regime in 2020. This post will look into the basics of income tax as well as the difference between the old and new regimes and the implications for taxpayers.

What is income tax?

Income tax is a direct tax levied upon an individual or organisation’s income or profits. To obtain the payable income tax, we multiply the income tax rate by the taxable income. Governments impose income taxes to meet various developmental objectives like:

- Equitable redistribution of wealth

- Social justice goals like allocation of resources to needier sections

- Funding various developmental and infrastructure projects

- Social security initiatives

Income tax becomes an important policy tool that governments use to direct certain financial and societal behaviours among firms and individuals. For example, governments provide some exemptions to encourage donations to charity.

How is income tax different from GST?

Income tax is a direct tax levied directly upon the income made by the assessee (the person who has to pay tax). GST, on the other hand, is an indirect tax levied on the production and sale of goods and services. GST is ultimately paid by the end consumer of the product or service.

Another significant difference is that while I-T is a progressive tax, GST is a regressive tax. This categorisation means that as the income slab rises, the tax rate also increases. Someone earning Rs 10L pays more income tax than someone who makes Rs 2L. However, the GST amount is constant for a given item regardless of the financial status of the person consuming it. So, a poor person pays a higher proportion of their income on GST than a richer person.

How does income tax work in India?

In India, income tax is paid annually by individuals, businesses, legally recognised persons, local authorities, and Hindu Undivided Families, etc., at a tax rate based on the slab under which their income falls. On behalf of the government, the Central Board of Direct Taxes collects the Income Tax. The fiscal year for tax collection in India is from 1st April of a calendar year to 31st March of the following calendar year.

The calculation of the income tax payable is not so simple as it sounds. First, one must calculate the taxable income, i.e., the net income after applicable exemptions and deductions. Then, the corresponding tax rate must be determined.

The net income is distributed into the different slabs for this calculation.

This means that if someone has a taxable income of Rs 5L, it would be distributed as follows:

Rs 0-2,50,000 at 0%

Rs 2,50,000-5,00,000 at 5%

Therefore, the tax payable would be just 5% of Rs 2,50,000= Rs 12,500

For salaried people, the employers do all this and deduct and pay the taxes directly (TDS). We have to file Income Tax Returns (ITR) that detail net income and deductions to get back refunds of excess tax paid.

Freelancers or business owners, on the other hand, have to calculate their advance tax payments as follows:

- Add all earnings from various sources—salary, rent, capital gains, etc., to estimate annual income.

- Subtract exemptions and deductions to get taxable income.

- Advance tax payable is calculated as the applicable slab percentages multiplied by taxable income.

Nowadays, it is possible to pay income tax online through the Tax Information Network of the I-T website.

Those who don’t know how to calculate their payable income tax can use online calculators available from reputed financial literacy websites. These calculators have various fields to give a hint of what to account for when calculating income tax.

How does income tax change every year? Difference between the Old Regime and the New Regime

The I-T system works, as mentioned above, with the principles remaining the same. What changes frequently is the tax rates at the different income slabs and the deductions available to different groups of people.

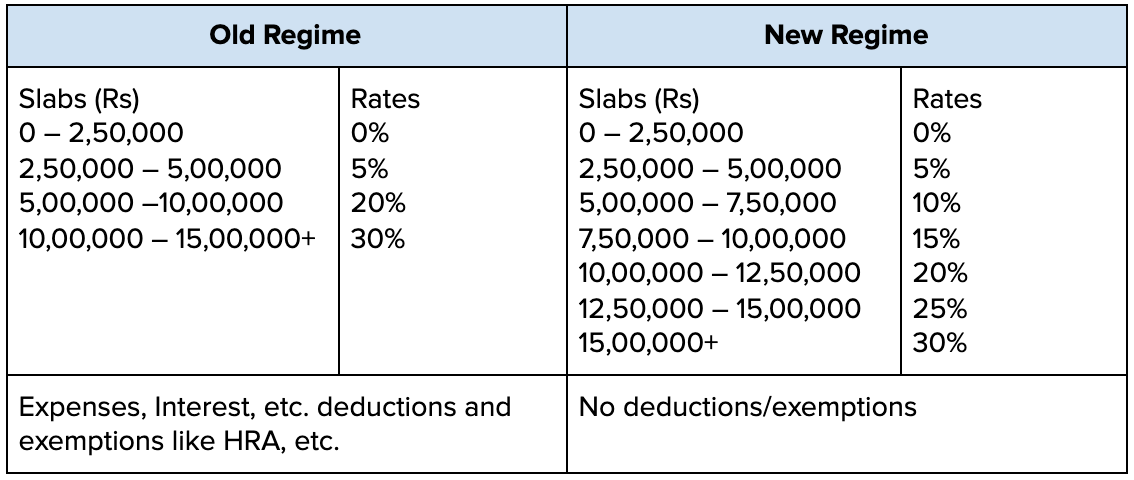

The Budget of 2020 brought some major changes in the Income Tax Regime and offered people the choice between paying as per the Old regime or the New regime. However, it is important to choose carefully as the choice cannot be changed later; the same regime will continue till year-end.

In the new regime, there are more tax slabs and lowered rates, but this comes at the cost of losing all the available deductions and exemptions. The Old Regime has about 70 exemptions and deductions giving taxpayers a lot of options to reduce their tax liability (the amount they owe to the I-T Dept.).

The table shows the differences between Old Regime vs. New Tax Regime for individuals

Thus we see that anyone who earns below Rs 15L can now break up the income into four new slabs at 10%, 15%, 20%, and 25%, respectively.

As seen above, there is no change in the lowest and highest tax slabs. There has been a 5% progressive increase in every next tax slab. Therefore, people belonging to the lowest tax slab will see no changes in their taxes. However, as taxes are calculated by splitting the income into every tax slab, those in the highest one can choose a regime based on their taxable income after applying the applicable exemptions.

Here is a non-exhaustive list of available deductions and exemptions:

- Standard deduction- Rs 50,000

- Sec 80C- up to Rs 1.5 L

- House Rent Allowance, rent paid, in the absence of HRA

- EPF

- Insurance- Life, Health

- NPS

- Repayment of education loan

- Interest payment of home loan

- Savings bank interest

- Medical expenses of disabled dependents and other medical expenses

- Charitable donations

How to make the best of the I-T system?

There is no single answer to the question of which regime is the best one to pick. The choice depends on the income and the applicable exemptions and deductions that we want to claim.

So, we should calculate the tax payable in both regimes and then choose the one where it is lower.

Although the New Regime removes all deductions and exemptions, it should not discourage people from making investments in various instruments like PPF, PF, life insurance, etc. These instruments give good interest rates that can maximise wealth and also provide social security.

Due to the coronavirus pandemic, the date for paying I-T and filing Income Tax Returns has been extended to Dec 31, 2020. Taxpayers whose accounts have to be audited have a longer deadline till January 31, 2021. We should make sure to stick to these deadlines as delays will attract interest payments.

Also read:

Presumptive Tax: Ways to File Returns & Save Taxes for Creative Professionals

Capital Gains Explained: Definition, Types, Exemptions & Tax Saving

Everything You Need to Know About PPF Account: Benefits & Features

Types of deductions under section 80C. What is included under 80C?

![Series Funding [Types, How it works and More!]](https://okcredit-blog-images-prod.storage.googleapis.com/2021/02/seriesfunding1.jpg)